What Are Investment Grade Bonds? Meaning, Benefits And Risks in India

Investment-grade bonds, as the name suggests, are suitable for investment purposes based on their lower risk characteristics compared to speculative or junk bonds. They are gaining popularity as they offer better returns on investments than traditional saving tools like fixed deposits, while at the same time having a limited risk of default.

Credit rating agencies accredit these bonds under the Securities Exchange Board of India (SEBI) regulations. Investment-grade bonds can be beneficial if you are looking for balanced investment opportunities. Before making the right investment choice, let us discuss all you need to know about these low-risk debt securities.

Investment Grade Bonds vs Other Fixed Income Options

To understand how these bonds compare to other popular fixed-income instruments, here’s a comparison across risk and liquidity factors:

| Feature | Investment-Grade Bonds | High-Yield Bonds | Fixed Deposits | Bond Mutual Funds |

| Risk Level | Low | High | Very Low | Moderate |

| Returns | Moderate (6 to 8%) | High (9 to 12%) | Low (5 to 6%) | Varies (6 to 10%) |

| Liquidity | Moderate | Low to moderate | High | High |

| Ideal for | Conservative investors | Aggressive investors | Risk-averse savers | Balanced Investors |

| Credit Rating Agencies Involved | AAA to BBB- | BB+ and below | Not rated | Depends on portfolio |

Characteristics Of Investment-Grade Bonds

These bonds provide excellent opportunities to earn passive income with a minimum risk of default. These bonds are issued by governments or corporations desiring to raise funds through debt financing. They are issued for a pre-determined tenure and yield to maturity.

Some of the critical characteristics of investment-grade bonds are:

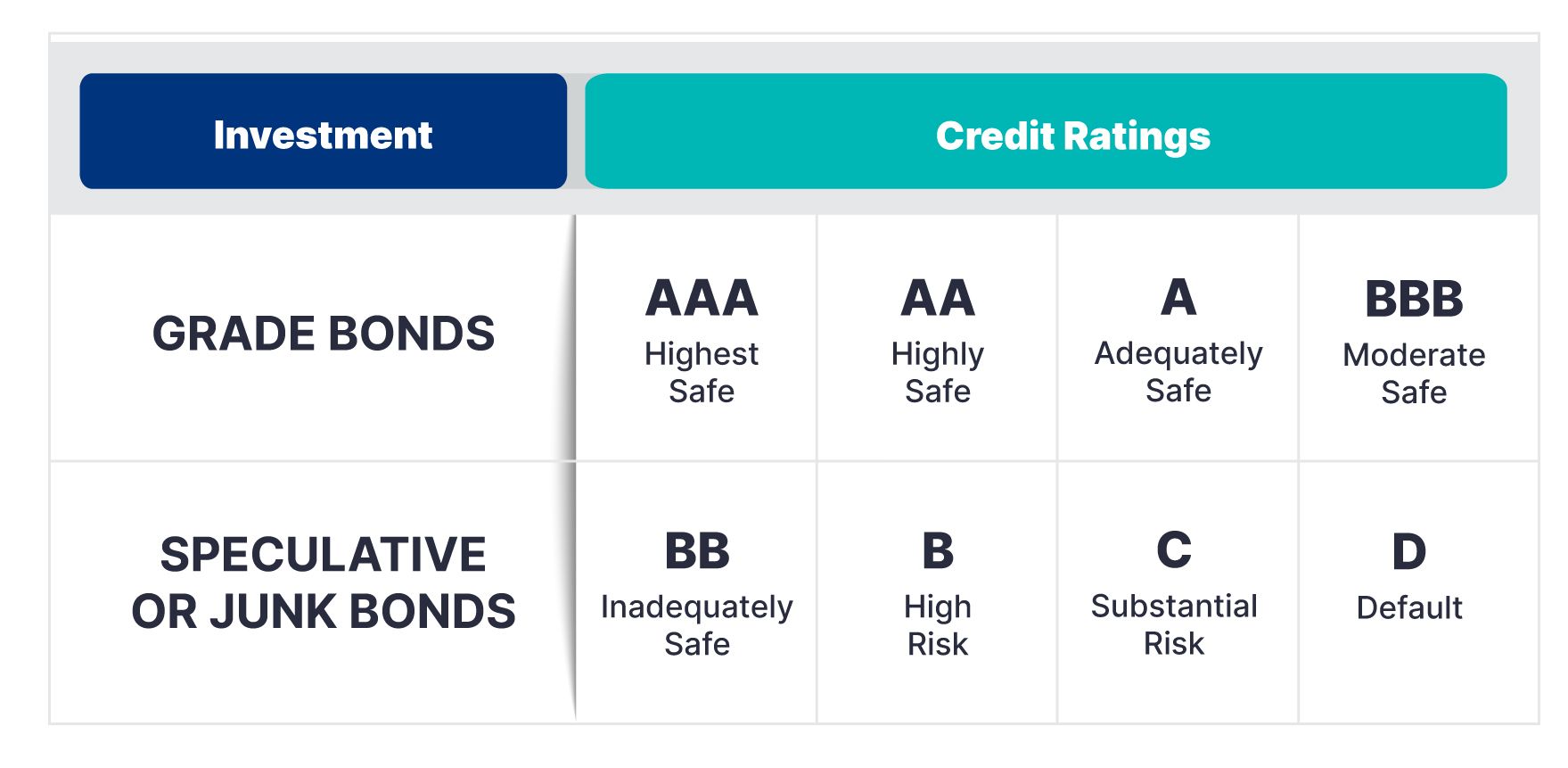

1. Credit Ratings

They are backed by the confidence of Indian credit rating agencies (CRAs). SEBI monitors these CRAs' standard operational procedures and implements timely updates to suit current market needs.

Demarcation of Investment-Grade Bonds As Per Indian Credit Rating Agencies

| Rating | Meaning | Risk Level |

| AAA | Highest quality | Very Low |

| AA | High quality | Low |

| A | Upper Medium Grade | Low to moderate |

| BBB | Medium grade | Moderate |

| BBB- | Lower end of investment grade | Moderate to slightly High |

2. Face Value

The face value of a bond refers to the price of a single unit of a bond issued by the company in the primary market. It is also known as a bond's principal, nominal, or par value. It is the value that the issuer is obligated to pay the investor back at maturity.

Face value differs from market value, representing the amount an investor has to pay to buy bonds in the secondary markets. Market value depends upon various economic factors, such as prevailing interest rates, changes in credit ratings, and demand and supply.

3. Tenure

The tenure of these secure bond offerings varies from a few months to 30 years. However, depending on the issuer, some bonds offer an option of early redemption after 3 to 7 years at a premature penalty.

Benefits And Risks Of Investment-Grade Bonds

The top-rated bonds offer the following advantages to investors:

- They are less risky than stock market investments.

- They offer stable, regular, and lower-risk passive income generation

- They provide higher returns than fixed-income alternatives like fixed deposits or sovereign gold bonds.

As the famous investor Warren Buffett once said, “Risk comes from not knowing what you are doing." The theory applies to high-grade bonds, too, as no investment is risk-free. Some of the risks and disadvantages involved with these assets are:

- Since the returns of investment-grade bonds are lower than those offered by stock markets (although at lower risks of default and volatility), an overallocation in these instruments may not be enough to generate the required returns to meet all your future needs.

- Bond investment comes with the restrictions of lock-in periods and low liquidity in secondary markets.

Example: Ramesh (45), a conservative investor from Mumbai, chose 3 bonds on Grip with AAA and AA ratings. His INR 1 lakh investment now generates INR 7,500 annually at a 7.5% YTM.

Also Read: Modified Duration Vs Macaulay Duration: Key Differences Every Bond Investor Should Know

Role In Portfolio Diversification

We have heard the saying “Never put all your eggs in one basket” millions of times when it comes to investing. Consequently, “portfolio diversification” aptly encapsulates the different investing instruments like equities/ mutual funds, bonds, fixed deposits, etc. Allocating funds to any or all of these opportunities requires careful consideration based on an investor’s income, age, risk appetite, and prediction of future needs.

With the advent of Online Bond Providing Platforms and stringent regulations laid down by the SEBI to protect retail investors’ sentiments, more investors are choosing investment-grade bonds over other fixed-income options. It allows them to take a balanced approach, spread between high-risk and high-yielding investments in stocks and parking of their savings in comparatively stable-grade debt instruments. The cherry on the cake comes from low-ticket size investment opportunities at these platforms, starting as low as INR 1,000. The feature allows retail investors to reap the benefits of high-growth investments.

Considerations For Investors

If you are planning to invest in investment-grade bonds, here’s a checklist for bond investing:

- Choose appropriate credit ratings based on your risk appetite. Remember: The higher the rating, the lower the risk of default.

- Choose a reliable investing platform that offers hassle-free operations and is regulated by the country’s governing body. Grip Invest, a SEBI-compliant online bond-selling platform, offers numerous curated investment opportunities.

- Before investing in corporate bonds of investment grade, assess your future requirements and invest only the amount you can lock in until maturity.

- Diversify within investment-grade bonds. If you want to cover all your bases and the stability of these low-risk fixed-income instruments attracts you, consider investing in multiple bonds with different characteristics.

Current Market Trends And Outlook On Investment-Grade Bonds

For any fast-paced, growing economy like India, a robust corporate bond market enables risk sharing with the banking system. According to the Bank of International Settlements, the escalating size of the Indian corporate bond market presents testimony to Indian regulators’ efforts toward stabilizing our economy1.

Investment-grade bonds are essential as Indian investors are inclined towards safer investment options. In FY22, the highest-rated bonds (AAA) accounted for 80% of issuance, followed by 15% investment in AA-rated bonds. According to SEBI, the outstanding stock of corporate bonds increased fourfold from INR 10.51 lakh crore in FY 2012 to INR 40.20 lakh crore at the end of FY 20222.

Although the issuer and investor base in investment-grade bonds keep rising with the GDP trends, we still lag behind our Asian counterparts. Therefore, the growth projections are riding on the improvement offered in reinforcing complementary markets, introducing better liquidity, and assuring easy access to investors.

Conclusion

Investment-grade bonds provide lucrative investment options for non-institutional investors. They are considered better yielding than fixed deposits and less risky than stocks and speculative bonds. Considering their benefits, these creditworthy bonds are the best solution for creating a balanced portfolio for long-term investors. Explore Grip Invest today and stay abreast with the latest information on the best investment opportunities.

FAQs On Investment Grade Bonds

1. How are investment-grade bonds different from high-yield or junk bonds?

Top-rated bonds are issued by financially stable entities with a lower risk of default. Junk bonds offer higher returns but come with higher risk. Credit ratings by agencies like CRISIL or ICRA help distinguish between the two.

2. Are investment-grade bonds safer than fixed deposits (FDs)?

Yes, these credit-rated debt securities generally offer better returns than FDs and maintain low risk. However, FDs are bank-backed and insured. On the other hand, bond investments depend on issuer credibility and may carry less liquidity.

References:

- Bank for International Settlements <https://www.bis.org/review/r220824c.pdf>

- Securities and Exchange Board of India <https://www.sebi.gov.in/statistics/corporate-bonds/outstandingcropbond.html>

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001